Home

Uncategories

If I Surrender My Life Insurance Is It Taxable / How To Calculate The Cash Surrender Value Of Life Insurance Life Settlement Advisors

If I Surrender My Life Insurance Is It Taxable / How To Calculate The Cash Surrender Value Of Life Insurance Life Settlement Advisors

If I Surrender My Life Insurance Is It Taxable / How To Calculate The Cash Surrender Value Of Life Insurance Life Settlement Advisors. Generally, life insurance proceeds you receive as a beneficiary due to the death of the insured person, aren't includable in gross income and you don't have to report them. Using life insurance policy loans to avoid taxes But if you cancel within the first few years of owning the policy, you'll have to pay fees and you might not get any money back. On january 1 of year 1, a, an individual, entered into a life insurance contract (as defined in § 7702 of the internal revenue code (code)) with cash value.under the contract, a was the insured, and the named beneficiary was a member of a 's family. The insurance policy at issue treated the capitalized interest as principal on the loan.

Life insurance proceeds are not taxable with respect to income tax, so long as the proceeds are paid out entirely as a lump sum, one time, payment. On january 1 of year 1, a, an individual, entered into a life insurance contract (as defined in § 7702 of the internal revenue code (code)) with cash value.under the contract, a was the insured, and the named beneficiary was a member of a 's family. A life insurance policy loan is not taxable as income, as long as it doesn't exceed the amount paid in premiums for the policy. If the csv is more than the premiums and you surrender the policy (cancel it), the excess is earnings and taxable. He would also owe taxes on $350,000.

What Is Cash Value Life Insurance Ramseysolutions Com from cdn.ramseysolutions.net If you later decide to surrender your policy, the gain can trigger a tax liability. Guaranteed surrender value is calculated using the formula: If the policyholder surrenders a cash value life insurance policy on his life for the cash surrender value, the excess of the cash surrender value of the policy over the tax basis (which equals what the policyholder has paid in premiums for the policy) equals ordinary income to the policyholder because the policy is not considered a capital asset. The cost basis of a life insurance policy is the sum of all your insurance premium payments. (note that outstanding loans are also counted as part of the gain.) You are allowed to surrender your policy at any time. My policy is about $190,000. On january 1 of year 1, a, an individual, entered into a life insurance contract (as defined in § 7702 of the internal revenue code (code)) with cash value.under the contract, a was the insured, and the named beneficiary was a member of a 's family.

Using life insurance policy loans to avoid taxes

You will pay tax on $2,000 at a rate of 25%. Using life insurance policy loans to avoid taxes (note that outstanding loans are also counted as part of the gain.) If the policyholder surrenders a cash value life insurance policy on his life for the cash surrender value, the excess of the cash surrender value of the policy over the tax basis (which equals what the policyholder has paid in premiums for the policy) equals ordinary income to the policyholder because the policy is not considered a capital asset. You are allowed to surrender your policy at any time. The insurance policy at issue treated the capitalized interest as principal on the loan. A had the right to change the beneficiary, take out a policy loan, or surrender the contract for its cash surrender value. You can generally expect to get a surrender charge within the first 10 or 20 years of owning the policy, and over the course of time the surrender charge phases out. When you cancel your whole life insurance coverage, you keep the cash surrender value of the policy. If you later decide to surrender your policy, the gain can trigger a tax liability. Guaranteed surrender value is calculated using the formula: Any amount withdrawn above the cost basis of a life insurance policy is taxable as ordinary income. There may be fees associated with your surrender, these are known as surrender charges.

However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit. A had the right to change the beneficiary, take out a policy loan, or surrender the contract for its cash surrender value. However, any interest you receive is taxable and you should report it as interest received. You pay $1,000 in surrender charges and receive a check from the insurance company for $12,000. (note that outstanding loans are also counted as part of the gain.)

Is Life Insurance Taxable In Canada Moneysense from moneysense.ca However, if you name yourself as the. However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit. You can generally expect to get a surrender charge within the first 10 or 20 years of owning the policy, and over the course of time the surrender charge phases out. A life insurance policy loan is not taxable as income, as long as it doesn't exceed the amount paid in premiums for the policy. If you pay for enough years, your policy builds up a cash surrender value, or csv. My policy is about $190,000. The funds you receive from the cash surrender value are taxable as ordinary income rather than capital gains. The cash you receive is untaxed, unless it exceeds the amount you paid towards your cash value.

A surrender does not affect your credit score, and a surrender will not affect your ability to get a new life insurance policy in the future (but changes in health can).

The funds you receive from the cash surrender value are taxable as ordinary income rather than capital gains. If you cash in a life insurance policy, you may need to pay tax on the cash surrender value. But if you cancel within the first few years of owning the policy, you'll have to pay fees and you might not get any money back. A life insurance policy loan is not taxable as income, as long as it doesn't exceed the amount paid in premiums for the policy. The cash surrender value in life insurance is only taxable on the amount over your basis. The internal revenue code provides that proceeds paid from an insurance company, when not part of an annuity, are generally taxable income for payments in excess of the total investment. You can generally expect to get a surrender charge within the first 10 or 20 years of owning the policy, and over the course of time the surrender charge phases out. Although you may owe income taxes if you choose to surrender your policy, policy payouts to a beneficiary are never taxable in the event of your death. To calculate your cash surrender value, take the total cash value (premiums you've paid minus the death benefit premiums) and subtract any surrender fees and charges the life insurance company charges (read the fine print on your policy). If emanuel canceled the entire policy, he'd receive $500,000 in cash from the life insurance company. However, if you name yourself as the. The special surrender value depends on the policy term, bonus (if any) and the number of premium installments the policyholder pays. You will pay tax on $2,000 at a rate of 25%.

If you make a partial withdrawal from a universal life policy, you incur no tax liability until you have withdrawn more from the policy than you have paid in premiums. However, if your beneficiary receives the life insurance payment as a series of installments, the insurer will typically pay interest on the outstanding death benefit. A mec is a term given. See topic 403 for more information about interest. To calculate your cash surrender value, take the total cash value (premiums you've paid minus the death benefit premiums) and subtract any surrender fees and charges the life insurance company charges (read the fine print on your policy).

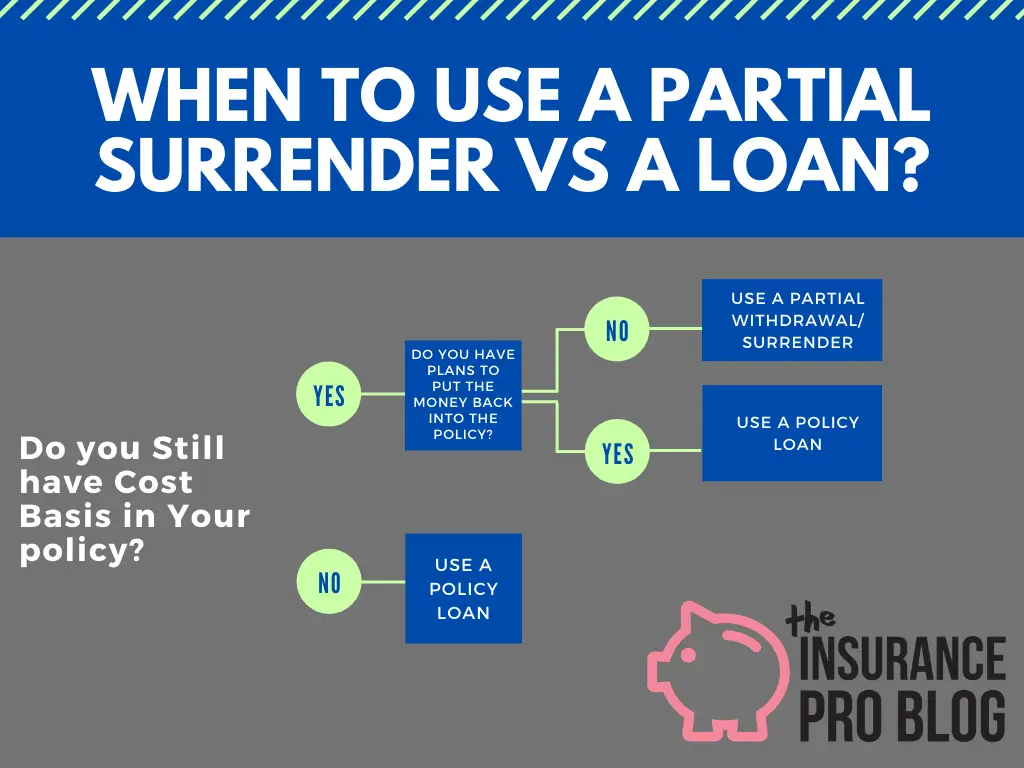

How To Do A Partial Surrender Of Your Life Insurance Policy from theinsuranceproblog.com (note that outstanding loans are also counted as part of the gain.) Any amount withdrawn above the cost basis of a life insurance policy is taxable as ordinary income. If you cash in a life insurance policy, you may need to pay tax on the cash surrender value. To calculate your cash surrender value, take the total cash value (premiums you've paid minus the death benefit premiums) and subtract any surrender fees and charges the life insurance company charges (read the fine print on your policy). If the policyholder surrenders a cash value life insurance policy on his life for the cash surrender value, the excess of the cash surrender value of the policy over the tax basis (which equals what the policyholder has paid in premiums for the policy) equals ordinary income to the policyholder because the policy is not considered a capital asset. The cost basis of a life insurance policy is the sum of all your insurance premium payments. If you pay for enough years, your policy builds up a cash surrender value, or csv. You pay $1,000 in surrender charges and receive a check from the insurance company for $12,000.

A had the right to change the beneficiary, take out a policy loan, or surrender the contract for its cash surrender value.

If you surrender your policy or your policy lapses, the loan (plus. However, if you want to determine your taxable distribution from the surrender ahead of time, the calculation is pretty simple. The cash you receive is untaxed, unless it exceeds the amount you paid towards your cash value. My question is about whole life insurance.my wife and i both have policies. Any amount withdrawn above the cost basis of a life insurance policy is taxable as ordinary income. If you make a partial withdrawal from a universal life policy, you incur no tax liability until you have withdrawn more from the policy than you have paid in premiums. By surrendering your policy, you will receive the current face value which includes both the premium payments along with any investment gains. If you pay for enough years, your policy builds up a cash surrender value, or csv. However, if you name yourself as the. On january 1 of year 1, a, an individual, entered into a life insurance contract (as defined in § 7702 of the internal revenue code (code)) with cash value.under the contract, a was the insured, and the named beneficiary was a member of a 's family. If you later decide to surrender your policy, the gain can trigger a tax liability. To calculate your cash surrender value, take the total cash value (premiums you've paid minus the death benefit premiums) and subtract any surrender fees and charges the life insurance company charges (read the fine print on your policy). He would also owe taxes on $350,000.

0 Comments:

Posting Komentar